MarketBullets®

See below for Chinese Yuan and Russian Ruble charts

Click HERE to return to Bullets

Base (non-annotated) Charts Courtesy of Genesis Trade Navigator.

Comment as of Friday, February 13, 2026

The Dollar Index (DX), is a multi-currency index. The Index does not include the Russian Ruble or the Chinese Yuan (Reminbi) among its components for calculation (see alt currency charts below).

Since mid-2022, the U.S. Dollar Index has been declining, but remains within a firmly defined 17-year upward channel. The current value is trading at about the same level as early 2022, which is just above the median value of the 40-year span back to 1986. It is hyperbole to claim that the Dollar is “weak”. It is lower than it was, but near the “normal” value in a wide historical range.

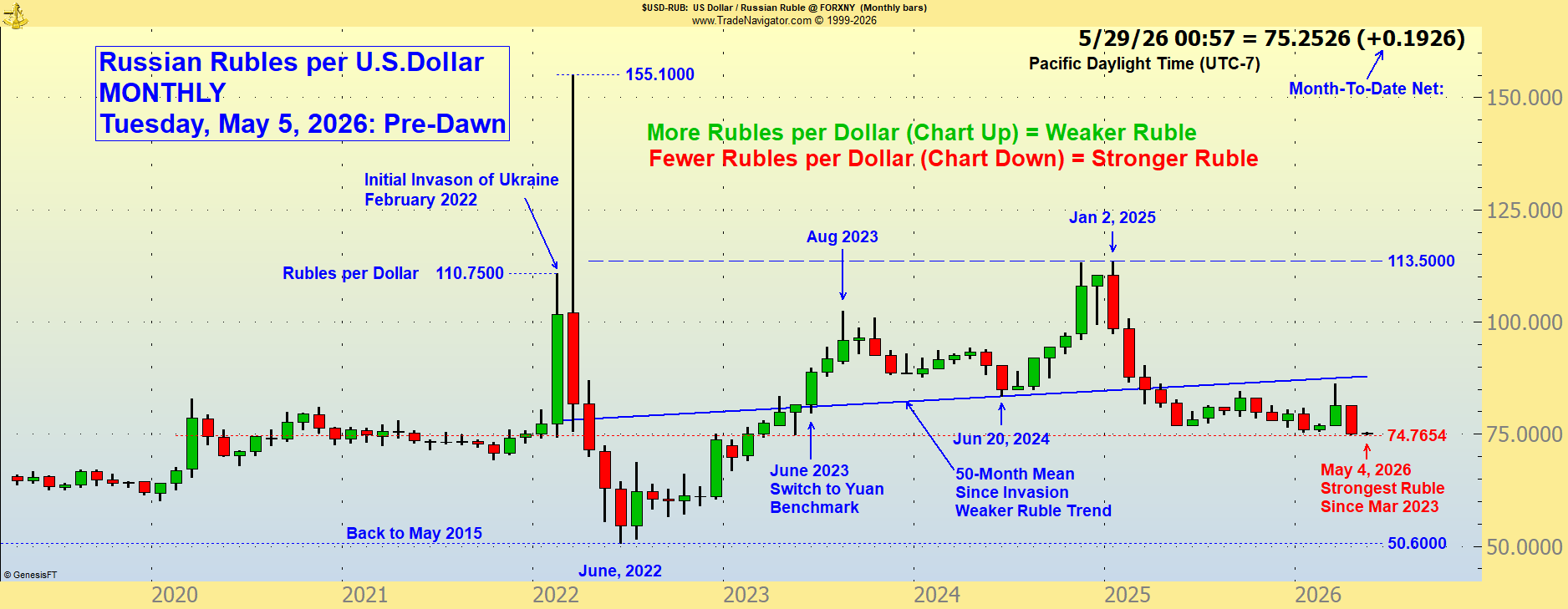

On June 12-13, 2025, the Russian government forced the U.S. Dollar off of Russia’s large central trading exchange (MOEX) in response to new international sanctions cutting Russia out of the “SWIFT” international trade settlement system. The Yuan is now designated as the Central Bank of Russia’s “Benchmark” currency. Anyone in Russia or dealing with Russia who wishes to use the USD for trade must use interbank markets instead of open exchange trades on the MOEX to price Rubles or Dollars, making it significantly more expensive and less transparent. The direct effect on the Dollar Index is not large. There are rumors that Russia may be interested in switching back into the U.S. Dollar market as a package of incentives designed to encourage U.S. lifting of sanctions (see comments under “Ruble”).

*A “Real Interest Rate” equals the observed market interest rate adjusted for the effects of inflation. The current nominal US Real Interest Rate is about +1.1%. The current rate of inflation as of February 13, 2026 is roughly 2.4%, while the yield on short-term treasury paper is from 3.4% to 3.6%. Currency flows tend to favor those that pay a positive real rate, but political and other risks are also taken into account. The long-term effect of perceived stability and safety along with positive rates is to make the U.S. dollar and/or government notes and bonds more attractive in global markets versus other currencies or paper, even of nations whose real interest rates are positive.

The U.S. Dollar Index is heavily weighted toward European currencies. The Chinese Yuan should be followed alongside the Dollar Index for a more complete assessment of Dollar value in the world. (see below)

Comment as of Wednesday, October 15, 2025

Over the last 2.5 years, Chinese Yuan versus the U.S. Dollar* has created a rising triangle, indicating a general long-term strength of the U.S. Dollar versus the Chinese currency. A flat top pattern with rising lows underneath sets up a test of the horizontal top line to the upside. This is an old-school rising pattern, but the breakout of the top flat line is essential for its success. If it “fails” due to a breakdown below the upward-slanted line (depicting increasing buying support over time), the pattern would be broken and invalidated. The Dollar value in Yuan is currently testing that rising line (stronger Yuan possible ahead).

The big-picture Yuan chart displays a long term rising Yuan per Dollar value (Weaker Yuan) back to 2014-15 during which the Chinese exercised a series of devaluations of their currency in an attempt to increase exports and move toward a market-oriented economy, a move that ultimately proved to be correct. The current dynamic of the Chinese currency is in a challenge to the reserve currency status of the U.S. Dollar.

* The above chart is a “dollar chart”, showing Yuan per US Dollar. A rising price indicates more Yuan per Dollar hence a less expensive Yuan.

Comment as of…Thursday

The Ruble is strengthening in a pattern that suggests intervention. The implications of a stronger Ruble start with a greater ability to purchase war-related goods, but a rising Ruble is also a factor in pricing wheat, putting pressure on the Russian producers to compare crops. There is already talk that wheat planting will be lower this year in areas where alternative crops can be grown.

The Ruble is responding to Ukraine status. It has become clear that Putin is unlikely to give any diplomatic ground at all with regard to Ukraine. The situation is emerging into “NATO versus Russia”, as the U.S. is taking a less visible role. The most recent blatant message from Moscow was the bombing of Ukrainian infrastructure within only a few hours after Putin had a long telephone visit with President Trump in which an “agreement”(?) was reached to cease such attacks for a month. The only response was “sanctions”. Putin has no reason to relent.

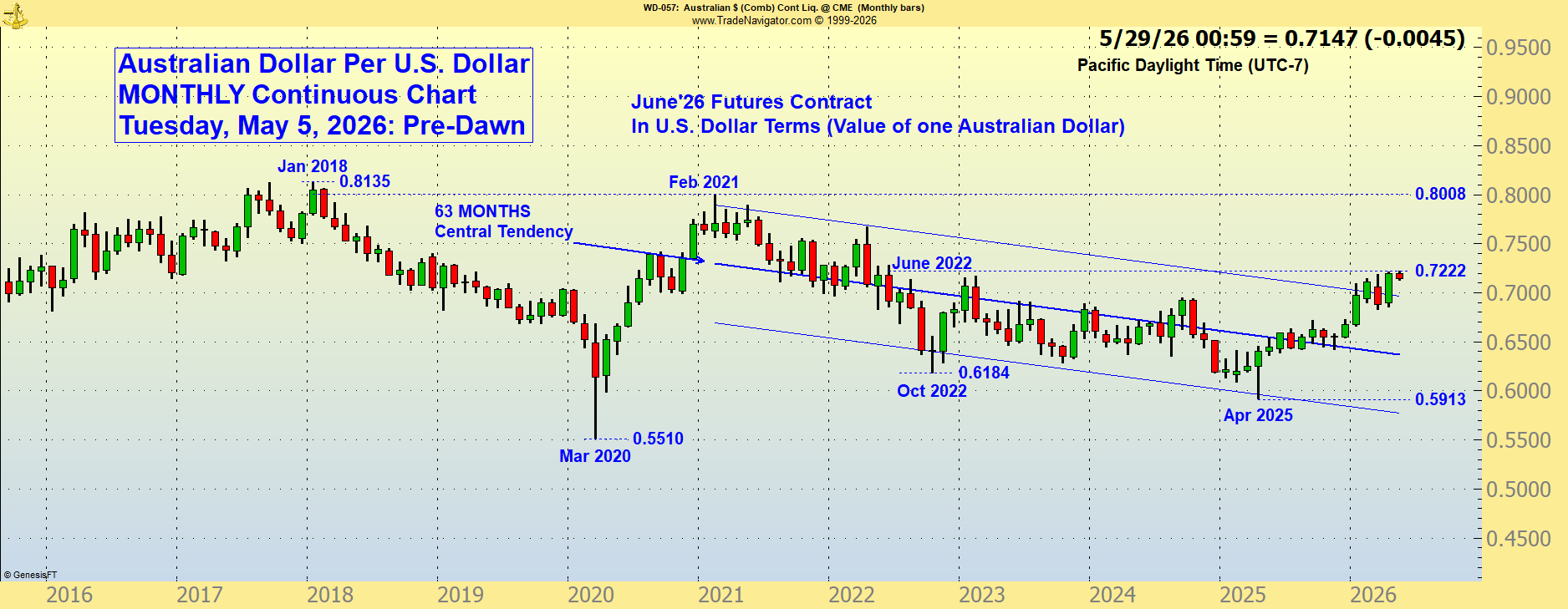

Australian Dollar

Click HERE to return to Bullets